Understanding bank fees can be confusing. Transactions usually go through smoothly, but a small mistake can lead to penalties, affecting your account. From common overdraft fees to less-known money transfer charges, these small fees can add up over time. One such confusing fee is the ACH Debit Return Charge for electronic payments. This article will explain what ECH/ACH Debit Return Charges are, when they are levied, and other important stuff you should be aware of.

Table of Contents

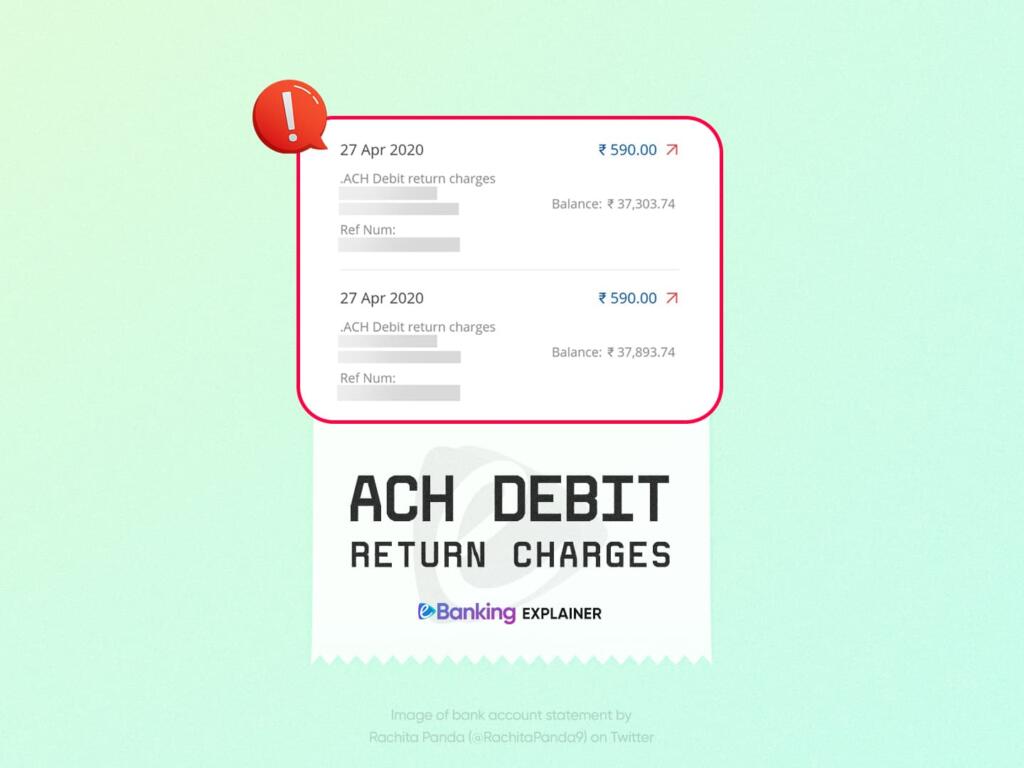

What are ACH Debit Return Charges?

Understanding ACH Debit Return Charges involves first understanding the concept of automatic electronic transactions. The ACH or ECH in these penal charges stands for Automated Clearing House or Electronic Clearing House. ACH/ECH is an electronic funds transfer system that facilitates the seamless automated transfer of money between banks and financial institutions. ACH/ECH is commonly used for various financial transactions, including direct deposits, payroll payments, bill payments, and electronic fund transfers. You might also be aware of terms like standing instructions or mandates where ACH is utilized.

An ACH Debit is a form of electronic transaction where the recipient (like a seller, lender, or service provider) has the authority to withdraw funds immediately from the payer’s (like a buyer or borrower) account, as and when the recipient requires. This mechanism is particularly useful for customers with recurring payments, offering a hassle-free way to settle bills automatically.

Various costs come into play to streamline the ACH debit payment process. Among them, the fee for initiating recurring transactions and the debit fee for each transaction are significant. Another aspect to consider is the cost associated with rejected/returned payments. Automatic payments can encounter obstacles for various reasons, such as insufficient funds in the sender’s account.

Other issues like inaccurate bank account information or frozen/dormant accounts can also lead to ACH transaction failures. In such cases, the Receiving Depository Financial Institution (RDFI) – the receiver’s financial institution, informs the Originating Depository Financial Institution (ODFI) – the payee’s financial institution, of the return or decline or bounce. This is when the ACH return charges are levied.

Why do ACH Debit Return Charges Occur?

As discussed above, automatic payments are prone to failures for multiple reasons, including lack of sufficient funds, holds or limits placed on accounts, incorrect account information, etc. When these ACH payments fail, banks levy the ACH Return Charges (ACH RTN or ECH RTN in short) as a penalty.

Two of the most common reasons for ACH Debit failures are:

- Insufficient Funds: One common reason for ACH Debit Return Charges is insufficient funds in the account. If your account balance is insufficient to cover the debit transaction, the bank may return the payment, accompanied by a charge.

- Suspended or frozen Account: In many cases, the payee’s account fails to honour ACH debit transactions due to the account being debit-frozen or suspended by the bank.

ACH Debit Return Charges can quickly add up, impacting your financial life. It’s essential to be aware of these charges to avoid unnecessary expenses. Repeated instances of ACH returns may lead to more severe consequences, including freezing your bank account. Therefore, one must keep track of their automatic recurring payments and be aware of the ACH Debit Return Charges for their accounts by referring to their bank’s terms and schedule of charges.

How to Avoid ACH Debit Return Charges?

We discussed the reasons banks charge ACH/ECH Debit Return Charges. Now, let’s explore what can be done to avoid these penal charges.

- Maintain Sufficient Funds: Regularly monitor your account balance to ensure there are sufficient funds in your account to cover your transactions.

- Ensure Account Health: Make sure that your bank account is not suspended or frozen by your bank. Be on the lookout for account-related communication from the bank in the form of messages, emails, and calls. Don’t hesitate to approach your bank if you feel something’s wrong with your account.

- Double-check Transaction Details: Double-check and verify all transaction details, including account numbers and IFSC codes, before initiating any electronic payment.

If you can’t maintain sufficient funds, or your account has some issues that might affect upcoming recurring payments, get in touch with the recipient and work on either cancelling or postponing the upcoming debit transaction. A stop order can be initiated to halt an ACH debit payment. This allows individuals to cancel the automatic payment by informing both the bank and the biller that they no longer wish to proceed with the payment. However, there is a specified time (normally around a week before the scheduled ACH debit, but may vary) until which stop orders can be initiated.

Can ACH Debit Return Charges be Reversed?

ACH debit return charges are typically challenging to reverse or waive. The associated debit return charges are applied once an ACH/ECH transaction has been declined or returned. Banks follow standard procedures and policies, and reversing these charges might not be straightforward.

However, there are cases where individuals can negotiate with their bank or financial institution, especially if the return was due to a genuine mistake or a one-time occurrence. It’s essential to communicate with the bank promptly, explain the situation, and inquire about the possibility of a reversal or refund. Sometimes, even expressing a willingness to close your bank account will also persuade banks to make an exception if you have a good standing relationship with them. Success in such requests may vary, often depending on the specific circumstances and the bank’s policies.

Some banks also have special banking programs or account variants where penal charges like ACH debit return charges are lower than other accounts or banks or are nil. For example, HDFC’s Imperia banking program is one such high-networth banking program with zero ACH debit return charges.

In conclusion, if you have already been charged the penalty, don’t hesitate to request your bank to reverse the same.

Frequently Asked Questions

Here are some of the most frequently asked questions on ACH RTN charges, answered:

-

What are ACH Debit Return Charges?

ACH Debit Return Charges are penal fees charged by banks when electronic transactions, like ACH debits, fail. Common reasons include insufficient funds or account issues.

-

How much is ACH Debit Return Charge?

The exact amount of fees varies from bank to bank. You can refer to your bank’s or account’s terms and schedule of charges documents to find out the exact ACH debit return charges.

-

How to avoid ACH Debit Return Charges?

ACH Debit Return Charges can be avoided by maintaining sufficient funds, ensuring account health, and double-checking transaction details. Initiate a stop order if needed, and communicate with your bank promptly.

-

How to reverse ACH Debit Return Charges?

Reversing ACH Debit Return Charges is challenging, but communicating promptly with the bank may help, especially for one-time errors. Success depends on the bank’s policies and individual circumstances.

Understanding ACH Debit Return Charges is vital for online transactions in India. We hope our explainer article helps you get behind the reasons and take precautions for a hassle-free banking experience. Let us know in the comments if you have any other queries, and we’ll try to help.

One Response

Sir,

Please guide

Daily Many ACH D debit clearing charges amount deducted in my account. I am not intrested ACH D. how to cancel this type of transaction. possible to re collect this money in my account

please guide me

Thanking You